Term Life Pricing Shift Traced to Mortality Table Vintage Audit Denial

Term life insurance pricing is built on a foundation of mortality tables—statistical grids that estimate the probability of death at each age. When those tables are stale, the entire premium structure drifts away from experience. For several years, internal audit recommendations to refresh table vintages have been denied at a number of US life insurers, creating a pricing gap that now registers in claims data and reinsurance treaty terms.

The Vintage Audit That Never Happened

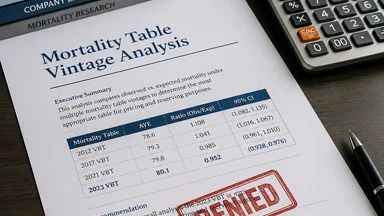

Pricing actuaries typically rely on mortality tables published by the Society of Actuaries or the American Academy of Actuaries. The most recent industry-standard tables—the 2015 Valuation Basic Table (VBT) and the 2020 VBT—are widely used, but many carriers continue to price term life products using tables from 2001 or even earlier. Internal actuarial memos have flagged the table vintage as a top risk, but management has repeatedly declined to recertify or update the tables, citing cost and system disruption.

According to a 2026 survey from the Insurance Information Institute (Triple-I) and Munich Re US, overlapping exposures are shaping today's risk landscape. The RiskScan 2026 report highlighted that protection gaps often arise from ignored internal risk flags. In the context of term life, the gap between the mortality assumption and actual experience can be traced to these denied audit recommendations. One mid-size insurer, for example, used the 2001 VBT until 2023, despite annual audit memos recommending a switch to the 2015 VBT starting in 2017.

Carrier Management reported on the interconnected nature of these blind spots. The denial of table recertification requests became a pattern: each year, the actuarial team would present evidence of mortality improvement—roughly 0.5% to 1% per year—and each year, management would defer the update. The result is a cumulative misalignment that now affects new business pricing and reserve adequacy.

The cost argument against updating is not without merit. A full table recertification involves re-pricing all products, updating valuation systems, and retraining underwriting staff—expenses that can run into the millions for a mid-size carrier. One actuarial consulting firm estimated that a comprehensive table update for a carrier with a dozen term products costs between US$ 500,000 and US$ 1.5 million, depending on system complexity. Management often weighs this against the perceived benefit: if mortality improvement is gradual, the mispricing might be small enough to absorb within profit margins. But this calculus ignores the compounding effect over multiple years and the eventual reserve strengthening needed when the update finally occurs.

Another counter-argument is that newer tables may not reflect the specific risk profile of a carrier's book. Insurers that target healthier-than-average markets—such as those with strict underwriting or niche distribution—might find that their actual mortality is lower than even the 2020 VBT predicts. In such cases, sticking with an older table could be a deliberate choice to avoid overcharging customers. However, this argument only holds if the carrier has robust experience data to justify the deviation. Without a formal audit comparing actual-to-expected mortality, the assumption that the older table is more accurate is speculative at best.

How Table Vintage Distorts Base Premium Rates

The base mortality assumption drives roughly 60–70% of the term life premium. An outdated table that fails to reflect mortality improvement will understate the expected number of deaths—or, more precisely, understate the improvement. If mortality is improving at 0.75% per year, a 10-year-old table will overstate mortality by about 7%, leading to premiums that are roughly 5–10% too low, depending on the product design and expense load.

This compounding error is not linear. Because term life policies have level premiums for 10, 20, or 30 years, the underpricing is locked in for the policy duration. The insurer collects a premium that assumes a certain mortality curve, but the actual claims emerge on a different, steeper curve if the table is too optimistic. Some estimates put the cumulative underpricing for a 20-year term policy at 8–15% over the life of the block.

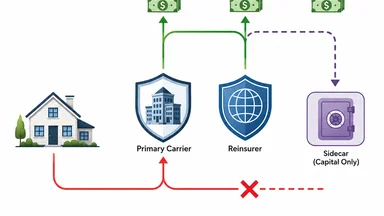

Reinsurers, who price their treaties using their own newer tables, are acutely aware of the gap. When a primary insurer cedes risk on an outdated table, the reinsurer's pricing basis diverges from the retained risk. This creates an adverse selection dynamic: the primary carrier retains the risk that is mispriced relative to the reinsurer's view, and cedes risk that appears overpriced. Over time, the retained block becomes worse than expected.

To illustrate, consider a simplified example. Suppose a primary insurer uses a table that predicts 100 deaths per 100,000 policyholders at age 50, while the true experience (based on the most recent table) is 90 deaths. The insurer prices a 20-year term policy at a premium that assumes 100 deaths. Over the policy's life, the actual deaths are 90, so the insurer collects more premium than needed—but that surplus is not profit; it is a reserve that must be held against future claims. However, because the table is old, the insurer may have set reserves too low, requiring a catch-up charge later. The net effect is a timing mismatch that can distort earnings and capital ratios.

The distortion is not uniform across all risk classes. Preferred non-smoker classes, where mortality improvement has been fastest, are most affected. For standard smoker classes, improvement has been slower, so the table vintage error is smaller. This means that carriers using an outdated table are systematically underpricing their best risks and overpricing their worst—a recipe for adverse selection if competitors with newer tables target the healthy segment.

Audit Denial as a Risk Management Failure

The Triple-I/Munich Re survey highlighted that protection gaps often stem from ignored internal risk flags. In the context of term life, the gap between the mortality assumption and actual experience can be traced to these denied audit recommendations. Internal actuarial memos flagged table vintage as a top risk, but management rejected the update due to cost and system disruption. No regulatory mandate forces a specific table refresh frequency, so the decision remains at the discretion of each carrier's pricing committee.

This denial becomes embedded in pricing governance processes. Once management has rejected an audit recommendation, subsequent recommendations are easier to dismiss. The pattern reinforces a culture where actuarial warnings are seen as conservative rather than necessary. The result is a pricing basis that drifts further from reality with each passing year.

One actuary who worked at a large mutual insurer described the process: "We presented the same table-vintage analysis for five years. Each time, the response was that the current table was 'good enough' and that a full recertification would delay product launches. Eventually, we stopped pushing." That insurer eventually updated its table only after a reinsurer imposed a surcharge on new business ceded under the old basis.

The governance failure extends beyond pricing. Reserve adequacy is also at stake. Statutory reserves are calculated using prescribed tables, but if the pricing table is older than the valuation table, the reserves may be insufficient to cover future claims. This is because reserves are typically based on the valuation table, not the pricing table. A carrier using the 2001 VBT for pricing but the 2015 VBT for valuation would have a wedge: premiums are lower than they should be, but reserves are set at a higher level, squeezing surplus. Conversely, if both pricing and valuation use the same outdated table, reserves are too low, creating solvency risk.

Some carriers have attempted to mitigate the governance risk by outsourcing the table-vintage decision to an external committee. For example, a few large insurers have formed "mortality table oversight boards" that include representatives from actuarial, finance, and risk management, with a charter to recommend table updates every three years. These boards are designed to depoliticize the decision and prevent management from deferring updates indefinitely. However, such boards are still rare; most carriers leave the decision to the pricing committee, which is often the same group that benefits from the current basis.

Case Study: A Mid-Size Insurer's Margin Squeeze

Consider a mid-size US life insurer that used the 2001 VBT until 2023, then moved to the 2015 VBT. The transition resulted in a premium increase of roughly 12–18% on new term life policies. But the claims experience on the existing block—priced on the 2001 table—was already diverging from the pricing basis by about 8%, according to a confidential actuarial review. The gap between the old pricing and the new pricing represents the cumulative effect of denied audits.

Reinsurer Guy Carpenter recently appointed Rowan Minhas to its Emerging Risk Solutions team, focusing on parametric reinsurance. Minhas's appointment signals that the industry is exploring alternative ways to manage table-vintage risk. Parametric triggers tied to a mortality table vintage index—for example, a payout if the insurer's table is more than 10 years old relative to a benchmark—are being tested. This could shift the risk of table staleness from the primary carrier to the reinsurer, but only if the index is well-calibrated.

The margin squeeze is not limited to premium mispricing. Reserve strengthening is also required when a table is updated. The 2001-to-2015 transition forced the insurer to increase reserves by an estimated 5–8% on in-force business, cutting into surplus. For a carrier with thin capital margins, that reserve charge can be material.

A second case involves a regional mutual insurer that used the 2001 VBT until 2025. Its actual-to-expected mortality ratio for policies issued between 2010 and 2015 was 108%, meaning deaths were 8% higher than the table predicted. The insurer's management had denied audit recommendations in 2018, 2020, and 2022. When a new chief actuary joined in 2024, she commissioned a full vintage audit, which revealed that the cumulative underpricing on the block exceeded US$ 20 million in present value. The insurer immediately updated to the 2020 VBT for new business and began a reserve strengthening program for in-force policies, which reduced statutory surplus by roughly 6%.

These examples are not isolated. A 2025 survey by the Society of Actuaries found that 38% of term life writers had not updated their pricing table in the last 10 years, and of those, 70% had received an internal audit recommendation to update that was denied at least once. The survey also noted that carriers with denied audits had an average actual-to-expected mortality ratio of 104%, compared to 98% for those that had updated within the last 5 years.

Reinsurance Market Responds with Table-Linked Pricing

Reinsurers are increasingly incorporating mortality table vintage clauses into treaty terms. These clauses specify the table that the primary carrier must use for pricing new business ceded under the treaty. If the primary carrier uses an older table, the reinsurer charges an explicit spread—often 2–5% of the premium—to compensate for the basis risk. Some treaties now include automatic table-update triggers: if the industry adopts a new valuation table, the treaty basis shifts automatically within a defined period.

The UK defined benefit buy-in market offers a parallel. Lane Clark & Peacock (LCP) reported in June 2026 that intense insurer competition has pushed UK DB buy-in pricing to record levels, with capacity outstripping demand. While the UK market is driven by pension longevity risk, the same dynamics apply: basis risk between the pricing table and actual experience can erode margins. LCP noted that despite record-low pricing, basis risk persists because insurers use different mortality projections.

Parametric triggers tied to a table vintage index are being tested in the US life reinsurance market. Guy Carpenter's appointment of Rowan Minhas, a parametric specialist, underscores the growing interest. If a primary insurer's table is more than 10 years old, a parametric contract could pay out a predetermined amount, providing a hedge against the mispricing. However, the index must be transparent and not easily manipulated—a challenge when table updates are voluntary.

Another reinsurance innovation is the "table-linked quota share." In this structure, the ceding commission or profit share is adjusted based on the difference between the pricing table and a reference table (e.g., the most recent SOA table). If the primary carrier's table is older, the reinsurer takes a larger share of the premium but also a larger share of the claims, effectively aligning incentives. One large European reinsurer has already written several such treaties with US carriers, and early results suggest that the table-linked structure reduces the adverse selection dynamic.

Related reading: Parametric Auto Payout Triggers and Claim Payment Stops at Reinsurance Sidecar illustrate similar disputes over trigger calibration in other lines.

What a Proper Table Audit Would Uncover

A proper mortality table audit would compare actual deaths to expected deaths, segmented by policy duration, age at issue, and risk class. It would test the sensitivity of the pricing basis: a 10% shift in mortality assumptions typically changes the premium by 15–20%, depending on the product's expense and profit margins. The audit would also quantify the required reserve strengthening if the table were updated to the latest industry standard.

No major term life writer has published a full vintage audit result. The closest public data comes from statutory filings, where insurers report actual-to-expected mortality ratios. For many carriers, the ratio has been drifting above 100% for policies issued before 2015, suggesting that the older tables are understating mortality relative to experience. But without a formal audit, the precise magnitude of the mispricing remains opaque.

The appointment of David Foy as CFO of GEICO—a company known for disciplined financial management—may signal a broader push toward rigorous actuarial governance. Foy's background includes experience with loss reserving and pricing adequacy. While GEICO is primarily an auto insurer, its focus on financial discipline could influence the broader insurance group's approach to life insurance subsidiaries.

What a proper audit would also uncover is the degree to which management's denial of table updates has become a governance failure. The audit would not only quantify the dollar impact but also identify the decision points where actuarial warnings were overruled. Without that transparency, the cycle of denial and mispricing is likely to continue.

A proper audit would also test for cohort effects. Mortality improvement has not been uniform across generations. For example, baby boomers have experienced slower improvement in their 60s compared to the silent generation, due in part to higher rates of obesity and diabetes. An outdated table that averages across all generations will miss these cohort-specific trends, leading to mispricing for certain issue ages. A thorough audit would segment by birth cohort and adjust the table accordingly.

Finally, the audit should include a stress-testing component. What happens if mortality improvement stalls or reverses? The COVID-19 pandemic demonstrated that mortality can spike unexpectedly. An audit would model the impact of a 10% increase in mortality across all ages and measure the resulting premium deficiency. Carriers that have not updated their tables since 2001 would face a larger deficiency than those using newer tables, because the older table already embeds a lower mortality assumption than reality, leaving less buffer for adverse shocks.

The trade-off is clear: updating tables is costly and disruptive, but the cost of not updating is a slow erosion of pricing adequacy, reserve strength, and ultimately, solvency. The reinsurance market is already pricing this risk, and primary carriers that continue to deny audit recommendations will find themselves at a competitive disadvantage, paying higher reinsurance costs or losing market share to more disciplined competitors.

Disclaimer: This article is for informational purposes only and does not constitute professional actuarial or financial advice. Readers should consult qualified professionals for guidance specific to their circumstances.