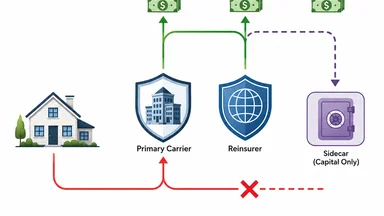

Long-Term Care Premium Flow Split Between US Self-Funded and German Pooled Reinsurance

Long-term care insurance sits at the intersection of life and health coverage, yet its premium mechanics vary dramatically across jurisdictions. In the United States, carriers typically retain 100% of the premium and bear the full weight of claims volatility. In Germany, a statutory pooled reinsurance system called the Pflegekasse absorbs catastrophic risk, fundamentally altering how premium dollars and euros flow. This article traces those flows, comparing the self-funded US model with Germany's mandatory cession structure, and explores what each approach means for reserve adequacy, profit stability, and reinsurance recoveries.

Why the Same LTC Policy Generates Different Premium Flows in the US and Germany

The core difference lies in risk retention. A US long-term care carrier collects a premium and holds the entire amount on its balance sheet. Roughly 85% of that premium goes to claims and reserves, with the remainder covering commissions, administrative expenses, and profit. The carrier prices based on its own morbidity tables, subject to state insurance department approval. If claims run higher than expected, the carrier must absorb the loss or seek a rate increase—a process that can take years and often faces political resistance.

In Germany, private LTC insurers must cede a portion of their premium to the Sozialen Pflegeversicherung (social long-term care insurance) pool. This mandatory cession covers catastrophic claims above a certain threshold. The reinsurance premium is roughly 2.5% of gross written premium, but the pool also receives a risk-adjustment transfer based on the insurer's age and gender mix. As a result, only about 60% of the premium funds claims directly; the remaining 40% flows to the pool or covers expenses.

The German model stabilizes carrier profits by capping downside risk. However, it also limits upside: efficient insurers with better-than-average morbidity cannot fully retain the benefit of low claims. The US model offers no such buffer, leaving carriers exposed to tail risk but allowing them to keep the full reward of favorable experience. This fundamental trade-off shapes everything from pricing strategy to reserve adequacy.

From a regulatory perspective, the US system relies on state-level solvency rules and stress tests, while Germany's federal law (SGB XI) mandates the pooled structure. The result is that a 65-year-old buying an LTC policy in Florida triggers a different premium flow than a 65-year-old in Bavaria, even if the underlying coverage is similar.

The US Self-Funded Model: Full Retention and Its Consequences

In the United States, no statutory reinsurance pool exists for long-term care. Carriers write policies, collect premiums, and establish reserves based on actuarial assumptions about morbidity, persistency, and interest rates. The National Association of Insurance Commissioners (NAIC) sets model regulations, but each state implements its own solvency requirements. Carriers must file rate increase requests with state regulators, a process that has become increasingly contentious as claim experience deteriorates.

Genworth Financial, once the largest US LTC writer, exemplifies the strain of full retention. Its legacy block of policies experienced claims roughly 40% higher than originally priced, leading to massive reserve charges and a near-collapse of the company's LTC business. The carrier sought multiple rate increases, but approvals came slowly and often below requested levels. By 2024, Genworth had stopped writing new individual LTC policies, shifting to hybrid life-LTC products instead.

The absence of a risk pool means US carriers must hold capital against extreme scenarios. Regulators require cash-flow testing and stress scenarios that include 20% claim spikes or 100-basis-point interest rate drops. Some carriers have responded by purchasing excess-of-loss reinsurance treaties from Bermuda-based reinsurers, covering claims above a retention—often around $500,000 per claim. However, these treaties are expensive and subject to annual renegotiation.

A related challenge is reserve adequacy. US GAAP accounting requires carriers to hold reserves equal to the present value of future benefits minus the present value of future premiums. If assumptions prove too optimistic, reserves must be strengthened, hitting earnings. Several carriers, including John Hancock and MetLife, have taken multi-billion-dollar reserve charges on their LTC blocks. The self-funded model concentrates this risk entirely on the primary carrier.

German Pooled Reinsurance: How the Pflegekasse Redistributes Risk

Germany's approach to LTC reinsurance is embedded in the statutory long-term care insurance system, established in 1995. Private insurers offering LTC coverage must participate in a risk pool managed by the Verband der Privaten Krankenversicherung (Association of Private Health Insurance). This pool, often called the Pflegekasse for private insurers, functions as a quota-share reinsurance mechanism with a risk-adjustment component.

Each insurer cedes a portion of its premium—roughly 2.5% of gross premium—to the pool. In return, the pool reimburses claims that exceed an annual threshold per insured, which as of 2024 is about €25,000. The pool also redistributes funds based on the insurer's risk profile: younger, healthier blocks subsidize older, sicker blocks. This equalization ensures that no carrier is penalized for attracting a less healthy population.

The effect on premium flow is significant. Instead of retaining 100% of claims, German insurers effectively retain only claims below the threshold. Above that, the pool absorbs the excess. This reduces the volatility of loss ratios and allows carriers to price with more confidence. However, the pool's premium is not risk-based in a traditional sense; efficient carriers subsidize less efficient ones, creating a moral hazard that regulators monitor.

From a reinsurance perspective, the German model functions as a mandatory quota-share treaty with a catastrophic excess layer. The pool's financial strength is backed by all participating insurers, making it a form of mutual reinsurance. Recoveries from the pool are typically processed within 30 days, far faster than the disputed treaty negotiations common in the US market. This speed reduces the need for carriers to hold large liquidity buffers.

Regulatory Divergence Drives Different Ceded Business Structures

The regulatory environment in each country directly shapes how LTC risk is ceded. In the US, state insurance departments focus on solvency and consumer protection, but there is no federal mandate for reinsurance pooling. Carriers choose whether to buy reinsurance based on their risk appetite and capital position. The result is a patchwork of excess-of-loss treaties, aggregate stop-loss covers, and, in some cases, no reinsurance at all.

Germany's federal law, Sozialgesetzbuch XI (SGB XI), mandates participation in the pooled reinsurance system for all private LTC insurers. This creates a level playing field: every carrier cedes the same proportion of premium and receives the same catastrophic protection. The system is administered by the PKV-Verband, which sets the cession rate and threshold annually based on industry-wide claims experience.

The divergence extends to reserve requirements. US carriers must hold reserves under statutory accounting principles (SAP) that are generally more conservative than GAAP. German insurers hold reserves under Solvency II, which includes a risk margin for non-hedgeable risks. Because the pool absorbs tail risk, German carriers can hold lower capital buffers for LTC than their US counterparts.

A practical consequence is that US carriers spend more on actuarial modeling and stress testing. They must demonstrate to regulators that they can survive a 1-in-200-year claims scenario. German carriers rely on the pool's diversification to reduce that requirement. The trade-off is that US carriers have more control over their underwriting and pricing, while German carriers accept the pool's standardized terms.

Premium Flow Comparison: Where the Dollar and Euro Land

Following the premium dollar through a typical US LTC policy reveals a flow: of every $100 in premium, roughly $70 to $80 funds claims and claim reserves. Another $15 to $20 covers commissions, underwriting, and administrative expenses. The remaining $5 to $10 is pre-tax profit, though this margin is highly variable by block and year. In a bad year, claims can consume 100% of premium, leaving carriers to draw down surplus.

In Germany, the euro flows differently. Of every €100 in premium, about €60 goes directly to claims and reserves for the portion of risk retained by the insurer. Approximately €30 is ceded to the Pflegekasse pool as reinsurance premium and risk-adjustment transfer. The remaining €10 covers expenses and profit. The pool's share includes the catastrophic layer, but also the cross-subsidy from younger to older insureds.

The profit margin for German carriers is narrower—typically 3% to 5% of premium—but more stable. The pool absorbs the volatility that would otherwise swing US carriers' results from year to year. German carriers also benefit from lower capital costs, as Solvency II capital requirements are reduced by the pool's risk absorption.

However, the German model caps upside. A carrier with exceptionally low claims cannot retain the full benefit; the pool recaptures some of the surplus through risk adjustment. In the US, a carrier with favorable experience keeps the entire margin, but must also bear the full cost of adverse experience. This asymmetry is a key consideration for actuaries designing products in either market.

Reinsurance Recoveries: Who Pays When Claims Spike

When a catastrophic claim event occurs—for example, a surge in dementia-related claims due to improved diagnosis—the recovery mechanics differ starkly. In the US, the carrier retains the first layer of claims, typically up to $500,000 per claim under an excess-of-loss treaty. Above that, the reinsurer pays, but only after a claims audit and often after disputes over definitions of "claim" and "trigger." Recoveries can take six months or more, straining the carrier's liquidity.

In Germany, the pool automatically reimburses claims above the annual threshold (about €25,000 per insured) without case-by-case review. The threshold is indexed to wage growth, so it rises over time. Recoveries are processed within 30 days, as the pool operates on a trust basis with standardized data feeds from carriers. This speed reduces the need for carriers to hold large cash reserves for unexpected claims.

The difference in recovery speed has implications for reserve adequacy. US carriers must hold higher reserves for incurred but not reported (IBNR) claims, as the delay in reinsurance recoveries increases uncertainty. German carriers can rely on the pool's prompt payment, allowing them to hold lower IBNR reserves relative to gross premium.

However, the German system is not without risk. If a catastrophic event affects the entire pool—such as a pandemic that increases LTC needs across all ages—the pool's capacity could be strained. In that scenario, the pool may increase the cession rate or reduce the threshold, passing costs back to carriers. The US system, by contrast, isolates each carrier's exposure, but at the cost of higher individual risk.

Practical Takeaways for Actuaries and Reinsurance Buyers

For US carriers, the key takeaway is that full retention demands robust modeling of tail risk. Stochastic scenarios that capture morbidity deterioration, interest rate shocks, and policy lapses are essential. Carriers should also consider purchasing excess-of-loss treaties with high retentions to protect against extreme outcomes, but should budget for potential disputes and slow recoveries. The experience of Genworth and others underscores that rate increases alone cannot fix underpriced blocks.

German insurers, by contrast, can rely on the pool to absorb volatility, but should monitor the pool's financial health and the risk-adjustment mechanism. If the pool's threshold is lowered or cession rate increased, profitability could compress. German actuaries should model scenarios where the pool's capacity is impaired, even if that risk seems remote. The stability of the German model is attractive, but it comes with less control over underwriting outcomes.

Cross-border lessons are instructive. The US could consider adopting a voluntary risk pool for extreme LTC claims, perhaps modeled on the German approach, to reduce the burden on individual carriers. Such a pool would require regulatory coordination and a funding mechanism, but could lower capital requirements across the industry. Conversely, Germany might explore allowing carriers to retain more risk in exchange for lower cession rates, incentivizing efficient underwriting.

Ultimately, the choice between self-funding and pooling depends on a carrier's risk appetite, capital position, and regulatory environment. Neither model is inherently superior; each reflects a different balance between risk retention and risk transfer. Actuaries and reinsurance buyers should consider their own block's characteristics and the stability of their reinsurance partners when designing LTC programs.

This article is for informational purposes only and does not constitute professional actuarial or financial advice. Specific reinsurance decisions should be made in consultation with qualified professionals.