Directors and Officers Policy Payout Delayed Over Board Meeting Minute Time Stamp

A directors and officers liability claim worth several million dollars has been stalled for more than a year because the time stamp on a set of board meeting minutes did not match the date the meeting supposedly occurred. The carrier, a specialty insurer focused on technology companies with annual revenues between $500 million and $2 billion, denied coverage on grounds that the minutes were created after a known loss event, making the policy application materially misleading. The policyholder, a publicly traded enterprise software firm with approximately $1.2 billion in annual revenue, filed a bad-faith lawsuit in federal court in late 2025. The case has not yet gone to trial, but discovery has already produced expert reports on document metadata that both sides say will determine the outcome. The dispute demonstrates how D&O carriers are using forensic tools to verify board records — and why a simple time stamp can become the centerpiece of a coverage fight.

The Claim and the Timestamp Gap

The claim arose from a shareholder lawsuit filed against the software firm's board of directors in early 2024, alleging that directors breached their fiduciary duties in approving a $300 million acquisition that later resulted in significant losses. The company tendered the claim to its D&O carrier, which had issued a three-year claims-made policy with a retroactive date of January 1, 2023. The carrier initially acknowledged receipt and began assigning defense counsel. Then, about six weeks later, it issued a reservation of rights letter that flagged potential issues with the board meeting minutes attached to the renewal application.

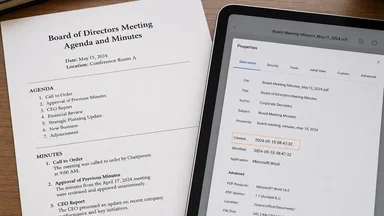

According to court filings, the minutes recorded a board meeting held by video conference on December 15, 2023. The meeting ostensibly approved the acquisition that later became the subject of the shareholder suit. The carrier's special investigation unit examined the PDF metadata and found that the document was created on January 10, 2024 — two days after the first shareholder demand letter was sent. The carrier argued that the minutes were backdated to create the appearance that the board had approved the transaction before any loss was foreseeable.

The policyholder countered that the minutes were drafted by the corporate secretary on January 10 but accurately reflected decisions made on December 15. The company's general counsel stated in a deposition that the secretary had been out sick during the week after the meeting and simply typed the notes later. The carrier rejected that explanation, citing a company policy that required minutes to be finalized within five business days. The claim was formally denied in March 2025.

The policyholder then sued for breach of contract and bad faith, seeking the full policy limit of $10 million plus consequential damages. The carrier moved to dismiss, arguing that the misrepresentation was material as a matter of law. The court denied the motion, allowing discovery to proceed on the issue of intent. Both sides have since deposed the corporate secretary and retained forensic document experts.

The board meeting in question was held via Zoom, a common practice for the company's quarterly meetings. The corporate secretary, who had been in the role for about 18 months, took handwritten notes during the call. She testified that she typed the formal minutes on January 10, 2024, because she had been on holiday from December 16 through January 2 and then spent the first week of January catching up on other tasks. She said she did not alter the content of the decisions, only formatted them for the official record.

The carrier's forensic expert, a former FBI digital forensics analyst, examined the PDF's metadata fields, including the document creation date, author name, and software version. The metadata showed the document was created using Microsoft Word 365 on January 10, 2024, at 2:47 PM. The expert also found that the document had been modified three times after that date, with the last save on January 12. The carrier argued that if the minutes had been drafted on December 15, the creation date would reflect that date or a date soon after.

The policyholder's expert countered that metadata can be altered or misread, and that the creation date in a PDF often reflects the date the file was exported, not when the content was written. He pointed to the fact that the minutes contained references to financial figures that were not publicly available until late December, suggesting the document could not have been created before that time — but he argued that this still supported the board's substantive decisions being made on December 15. The court allowed both experts to submit reports and scheduled a Daubert hearing for mid-2026.

The gap between the meeting date and the minute creation date — roughly three weeks — is not unusual in practice. Many corporate secretaries finalize minutes days or weeks after a meeting, especially when travel or holidays intervene. But the carrier's underwriting guidelines, which the company had signed off on during the application process, required that minutes be kept contemporaneously. The policy itself did not define "contemporaneous," but the application questionnaire asked whether the company maintained "current and accurate" board records. The company answered yes.

The Legal Tactic: Rescission vs. Coverage Denial

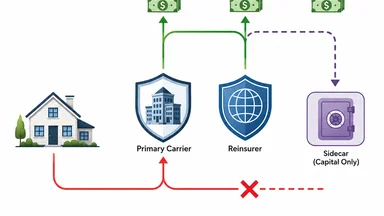

The carrier did not simply deny the claim; it sought rescission of the entire policy, arguing that the misrepresentation about the minutes was material to its decision to issue coverage. Rescission is a remedy that voids the policy ab initio, meaning it is treated as if it never existed. If successful, the carrier would owe nothing — not even defense costs already advanced. The policyholder has vigorously opposed rescission, calling it a disproportionate penalty for what it describes as a minor administrative lapse.

Federal courts in several circuits have split on the standard for rescission in D&O cases. Some require the insurer to show that the misrepresentation was both material and intentional, while others apply a strict-liability standard for statements in the application. The policy at issue contained a standard integration clause stating that the application formed part of the policy. The carrier argued that any false statement in the application, even if unintentional, could support rescission under the state's insurance code. The policyholder cited a recent appellate decision from the same state that required a showing of scienter.

The court has not yet ruled on the rescission issue, but discovery has focused heavily on the corporate secretary's state of mind. Emails produced in discovery show that the secretary emailed the draft minutes to the general counsel on January 10 with the subject line "Draft minutes from Dec. 15 meeting — sorry for the delay." The general counsel replied "Looks fine, thanks" without noting the delay. The carrier's attorneys have pointed to the absence of any apology or explanation in the secretary's email as evidence that she knew the minutes were late and tried to conceal it. The policyholder argues that the email itself shows transparency.

A similar case from the Southern District of New York, cited by both sides, involved D&O rescission over board minutes that were created after a lawsuit was filed. In that case, the court denied rescission because the insurer could not prove the policyholder intended to deceive. But the court noted that the outcome might differ if the minutes were created after the claim was tendered. Here, the minutes were created before the claim was tendered but after the first demand letter. The carrier argues that the demand letter constituted a "claim" under the policy's notice provisions, triggering the duty to notify the carrier immediately.

The legal arguments also touch on the concept of materiality. The carrier contends that the timing of the minutes is material because it goes to the board's oversight and the accuracy of the application. The policyholder counters that the minutes accurately reflect the board's decisions, and any delay in drafting is irrelevant to the risk assumed by the carrier. The court's ruling on this point could set a precedent for how similar disputes are resolved.

Why D&O Carriers Scrutinize Board Records

D&O carriers have long reviewed board minutes as part of underwriting, but the intensity of that review has increased in recent years. Post-loss underwriting audits — where carriers re-examine application materials after a claim is filed — have become standard for large D&O exposures. Special investigation units now routinely include forensic document analysts who can detect anomalies in timestamps, metadata, and even the font consistency of scanned documents. The goal is to identify any discrepancy that could support a rescission or coverage denial.

Industry data, while not publicly audited, suggests that roughly 12 percent of D&O claim denials involve some form of document-related issue, according to a 2024 survey by a major brokerage. That figure includes missing minutes, unsigned resolutions, and timestamp gaps. The percentage is higher for claims involving merger objections or shareholder derivative suits, where the timing of board actions is often central to the underlying liability. Carriers argue that they are not looking for minor administrative errors but for patterns that suggest the board was not properly informed at the time of a decision.

Fraud rings have also exploited D&O policies by fabricating board records to support inflated claims. In one documented case from 2023, a group of executives created retroactive board minutes to claim they had approved a transaction that later failed, generating a loss they sought to recover under their D&O policy. The carrier's SIU uncovered the scheme through metadata showing the minutes were created after the loss occurred. The ring was indicted for insurance fraud, and the carrier avoided paying the claim. That case sent a signal to the industry that board records could no longer be taken at face value.

As a result, adjusters and SIU investigators now receive training on how to verify meeting documentation. They look for consistent formatting across minutes, logical sequence of dates, and evidence of electronic signatures. Some carriers have begun requiring that board minutes be uploaded to a secure portal within a set number of days after a meeting, with automated time stamps. The technology firm in the current dispute had no such system in place.

Aon's Middle Market Chief Broking Officer Notes Trend

Lauren Pratscher, who joined Aon as Chief Broking Officer for its middle market P&C operations in June 2026, has observed increased carrier scrutiny of board records among mid-sized companies. In a recent interview with ReinsuranceNe.ws, she noted that brokers are now advising clients on minute-keeping practices as part of the pre-binding process. "We are seeing more pre-binding audits where the carrier asks for a sample of board minutes from the past year," Pratscher said. "If the minutes are sloppy or missing, the carrier may decline to quote or add an exclusion."

Pratscher's comments reflect a broader shift in the middle market, where D&O coverage was once relatively easy to obtain. She emphasized that the trend is not limited to large public companies. Private companies with outside directors, venture-backed startups, and nonprofit boards are all facing similar scrutiny. Aon's middle market unit has developed checklists for clients to use when preparing board materials, including reminders to date-stamp documents and retain meeting recordings.

The broker's role in this environment is to help policyholders understand what carriers are looking for before a claim arises. Pratscher noted that many companies do not realize that a routine administrative delay — like a secretary taking three weeks to type minutes — can become a coverage issue. She recommended that companies adopt real-time minute-taking practices, using collaborative tools that automatically log creation and edit times. "The carrier is not your adversary during underwriting," she said. "But if you give them a reason to doubt the accuracy of your records, they will use it."

The technology firm in the current dispute had engaged a retail broker who did not flag the minute-keeping issue during the application process. The firm's general counsel acknowledged in a deposition that he had never reviewed the carrier's underwriting guidelines regarding board records. The broker is not a party to the lawsuit, but the policyholder has considered filing a professional negligence claim against the brokerage.

Practical Safeguards for Policyholders

Companies seeking D&O coverage — or already holding it — can take several steps to reduce the risk of a timestamp-related dispute. The first is to adopt real-time minute-taking with digital signatures. Tools like Diligent or BoardEffect allow board members to review and approve minutes electronically, with an audit trail that shows when each person signed. Some carriers now prefer or even require such platforms for companies above a certain revenue threshold.

Second, companies should maintain a clear audit trail for all board materials. This includes saving meeting agendas, presentations, and any resolutions passed during the meeting. If minutes are drafted after the fact, the drafter should note the original meeting date and the date of drafting in the document itself. The policyholder in the current dispute did not include such a notation, which the carrier's expert cited as evidence of intent to mislead.

Third, companies should notify their D&O carrier immediately upon receiving any demand letter or lawsuit, even if they believe the claim is groundless. The policy at issue required notice "as soon as practicable" after a claim is made. The carrier argued that the company's failure to notify until after the minutes were created constituted a separate breach of the policy. The court has not yet ruled on this issue, but it illustrates how notice timing can intersect with document creation.

Fourth, companies should review their D&O policy's notice provisions with legal counsel before a claim arises. Many policies require that the application be attached and incorporated by reference, meaning any misstatement — even an unintentional one — can be used to deny coverage. A proactive review can identify potential gaps, such as the lack of a definition for "contemporaneous" minutes, and allow the company to negotiate clearer language at renewal.

The Bigger Picture: Precision as Coverage Currency

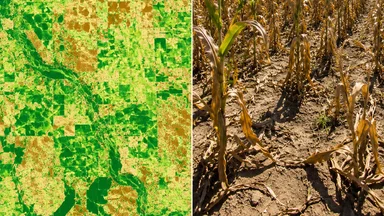

The dispute over the board meeting minute time stamp is not an isolated incident. It reflects a broader trend in which metadata and document forensics are becoming central to claims disputes across multiple lines of insurance. Auto telematics claims, for example, often turn on GPS timestamp logs. Crop insurance disputes hinge on satellite vegetation index data. Health plan premium audits rely on diagnostic code audits. In each case, the precision of digital records determines whether a claim is paid or denied.

Courts are increasingly split on how to handle rescission remedies in these cases. Some judges view rescission as a harsh penalty that should be reserved for intentional fraud. Others see it as a necessary tool to maintain the integrity of the underwriting process. The outcome of the current case could influence how D&O carriers approach minute verification in the future. If the court denies rescission, carriers may tighten policy language to define "timely" notice and "contemporaneous" records more explicitly.

Policy language is already evolving in response to these disputes. Some carriers have introduced endorsements that require policyholders to certify the accuracy of board records on a quarterly basis. Others have added exclusions for claims arising from transactions approved at meetings where minutes were not finalized within a specified period. These changes shift the burden of proof onto the policyholder, making it harder to argue that a timestamp gap was harmless.

For now, the technology firm's D&O claim remains in limbo, with legal costs mounting on both sides. The carrier has spent an estimated several hundred thousand dollars on forensic experts and outside counsel. The policyholder has incurred similar expenses, plus the cost of defending the underlying shareholder suit without carrier-funded counsel. Neither side appears close to settlement. The case is scheduled for trial in early 2027, unless a dispositive motion resolves it sooner.

Looking ahead, the industry may see more standardized requirements for board documentation, perhaps through model legislation or NAIC guidelines. Alternatively, carriers might develop proprietary software that integrates with corporate governance platforms to automatically timestamp and store minutes. Either way, the era of casual minute-keeping is ending. For policyholders, the lesson is clear: precision in board records is no longer just good governance — it is a prerequisite for coverage.

This article is for informational purposes only. It does not constitute legal or insurance advice. Readers should not rely on any recommendations herein without consulting qualified professionals regarding their specific circumstances. The author and publisher disclaim any liability for actions taken based on this content.