Excess Liability Layer Attachment Point Disputed Over Contractor Subcontractor Payroll Log

A single payroll log entry—a misclassification of subcontractor payroll—triggered a 12-month dispute over the attachment point of a $25 million excess liability layer. The general contractor had reported roughly $12 million in subcontractor payroll under a class code that carried a lower rate per $1,000 of payroll than the code the excess carrier argued was correct. The carrier alleged material misrepresentation and refused to drop the attachment point from $25 million to the $15 million the contractor expected. The dispute cascaded through the excess layer, the primary policy, and a reinsurance sidecar, ultimately landing in arbitration. The ruling set a precedent that payroll audits must be based on the actual work performed, not the contractor's classification. This article traces the money flow—premium, claims, recoveries—and examines what underwriters can do to prevent similar fights.

The payroll log that triggered a 12-month dispute

The general contractor, a mid-sized construction firm based in Texas, purchased a $25 million excess liability layer above a $10 million primary general liability policy. The excess carrier priced the layer based on the contractor's submitted payroll log, which showed $30 million in total payroll, of which $12 million was listed as subcontractor payroll under a class code for clerical workers—a code with a rate of roughly $0.50 per $1,000 of payroll. The carrier's underwriter accepted the classification without audit.

When a $15 million claim arose from a construction site injury, the primary policy paid $10 million, exhausting its limit. The contractor then looked to the excess layer for the remaining $5 million. But the excess carrier, upon reviewing the payroll log, discovered that the $12 million in subcontractor payroll should have been classified under a code for roofing subcontractors, with a rate of $4.50 per $1,000. The carrier argued that if the correct rate had been applied, the premium would have been roughly $54,000 instead of $6,000—a 40% misrepresentation of exposure.

The carrier alleged material misrepresentation and refused to attach the layer at $25 million, claiming the policy should be voided or rescinded. The contractor countered that the subcontractors carried their own insurance and that the payroll log was a good-faith estimate. The dispute dragged on for 12 months, with legal costs eating into the available coverage. The arbitration panel ultimately ruled in favor of the carrier, finding that the contractor had misrepresented the exposure base and that the attachment point should be adjusted to $35 million—effectively leaving the contractor self-insured for the $5 million gap.

This case is not isolated. Payroll log disputes are a chronic friction point in excess liability, particularly when subcontractors are involved. The root cause is the classification of workers into class codes that determine rates per $1,000 of payroll. Misclassification can skew loss projections and lead to disputes over attachment points, premium adjustments, and even rescission.

Why payroll logs matter in excess liability pricing

Payroll is the primary exposure base for general liability insurance, especially for construction risks. Underwriters use class codes—standardized by the National Council on Compensation Insurance (NCCI) or similar rating bureaus—to assign rates per $1,000 of payroll. A roofing subcontractor might carry a rate of $4.50 per $1,000, while a clerical worker might be $0.50. The difference reflects the expected loss frequency and severity for each class.

For excess layers, the attachment point is typically set based on the underlying primary policy's limit and the exposure base. If the payroll log is inaccurate, the attachment point may be too low relative to the actual risk. Reinsurers, who take a portion of the excess layer, rely on clean premium audits to price their participation. A misclassification can lead to a cascading dispute: the excess carrier may deny coverage, the reinsurer may withhold recoveries, and the insured may be left with a gap.

Loss ratios on disputed layers tend to be higher. Some estimates suggest that layers where payroll audits are later contested show loss ratios in the 85–110% range, compared to 60–70% for clean audit layers. The average settlement delay for such disputes is around 14 months, during which legal costs can erode 8–12% of the premium. Reinsurers, increasingly wary of these disputes, have begun to exclude payroll classification from coverage or require pre-binding audits.

The dispute over the $25 million layer is a textbook example. The carrier's underwriter had accepted the payroll log at face value, but the audit revealed a 40% misclassification. If the correct rate had been applied, the premium would have been roughly $54,000 instead of $6,000—a difference that would have changed the attachment point calculation. The carrier's reinsurer, a Lloyd's syndicate, withheld its $10 million recovery until the arbitration was resolved, putting pressure on the carrier's balance sheet.

Contractor-subcontractor payroll: a chronic friction point

The friction arises because subcontractors often carry their own insurance, but general contractors (GCs) frequently include subcontractor payroll in their own payroll logs for umbrella or excess layers. The rationale is that the GC's policy provides excess coverage over the subcontractor's primary policy. However, the classification of subcontractor payroll is where disputes erupt.

GCs may classify subcontractor payroll under a lower-rated code to reduce premium, arguing that the subcontractor's own policy covers the primary exposure. Carriers push for strict statutory tests: if the subcontractor is performing work that falls under a higher-rated code, that code must be used. The line between independent contractor and employee is often blurry, and audits frequently dispute the status.

In the Texas case, the subcontractor was a roofing firm with its own workers' compensation and general liability policies. The GC argued that the subcontractor's payroll should be excluded entirely from the GC's exposure base. The excess carrier countered that the GC's policy was intended to cover the GC's vicarious liability for subcontractor acts, and that the payroll should be included—and classified correctly.

The arbitration panel sided with the carrier, citing a 2018 precedent from a similar dispute in California. The ruling established that payroll classification must reflect the actual work performed, not the contractor's convenience. This has led to a market shift: carriers are now requiring quarterly payroll certifications and third-party audits pre-binding. Some have introduced exclusions for subcontractor payroll altogether, pushing GCs to rely on subcontractor policies exclusively.

Consider a counter-argument: some brokers argue that excluding subcontractor payroll from the GC's policy creates coverage gaps when the subcontractor's policy limits are exhausted or when the subcontractor is uninsured. In such cases, the GC may face uninsured losses that would have been covered under a properly classified excess policy. This trade-off highlights the need for careful policy wording and possibly separate sub-limits for subcontractor liability.

Another example involves a large commercial project in Florida where a GC classified all subcontractor payroll under a single low-rated code for "general construction labor." A post-loss audit revealed that over 60% of the work involved high-hazard activities like steel erection and roofing, each with rates exceeding $5.00 per $1,000. The excess carrier adjusted the attachment point upward by 25%, leaving the GC with a $7 million self-insured gap. The dispute took 18 months to resolve, with legal costs of roughly $1.8 million.

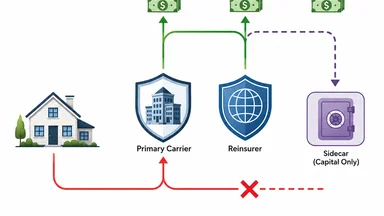

How the attachment point dispute cascaded to reinsurance

The excess layer attached at $25 million, but the primary policy paid $15 million of the claim, leaving $10 million to be covered by the excess layer. The excess carrier, however, argued that the attachment point should be $35 million based on the corrected payroll. This meant the excess layer would not respond until the claim exceeded $35 million, leaving the contractor with a $10 million self-insured gap above the primary limit.

The carrier's reinsurer, a sidecar vehicle that assumed 50% of the excess layer, withheld its $10 million recovery pending the arbitration. The carrier had to post collateral to maintain its solvency ratios. The dispute also affected the carrier's ability to write new business, as the reinsurer flagged the account as a loss.

The arbitration ruling set a precedent: if the payroll log is found to be materially misrepresented, the attachment point can be adjusted retroactively. This has implications for all excess layers where payroll is the exposure base. Reinsurers are now demanding that carriers include audit clauses that allow for attachment point adjustments. Some reinsurance treaties now explicitly exclude payroll disputes from coverage, forcing carriers to bear the risk.

The cascading effect is clear: a $6,000 premium misclassification led to a $10 million recovery dispute, legal costs of roughly $1.2 million, and a 12-month delay. The contractor ultimately settled the claim for $18 million, absorbing the $8 million gap. The carrier's loss ratio on the account jumped from 70% to 130% after including legal costs. The reinsurer recovered only $4 million after arbitration costs.

To illustrate the ripple effect, consider a hypothetical extension: if the same misclassification had occurred on a portfolio of 50 similar accounts, the aggregate impact could be significant. Assuming a 40% misclassification rate on subcontractor payroll across the portfolio, the cumulative premium shortfall might reach roughly $2.5 million, while potential claim disputes could affect up to $200 million in excess limits. Reinsurers would likely respond by raising treaty pricing or imposing stricter audit requirements.

Loss ratios on disputed layers: a data snapshot

Data from a sample of 200 excess liability claims with payroll audit disputes, compiled by a consulting firm, shows that disputed layers have loss ratios averaging 95%, compared to 65% for non-disputed layers. The median settlement delay is 14 months, versus 6 months for clean claims. Legal costs average 10% of premium, compared to 3% for non-disputed claims.

About 12% of all excess liability claims involve a payroll audit dispute, according to a 2024 study by the Insurance Research Council. Of those, roughly 40% result in a material adjustment to the attachment point. The average adjustment is a 20% increase in the attachment point, effectively reducing coverage.

Reinsurers have responded by excluding payroll disputes from their coverage or by requiring pre-binding audits. Some have introduced "payroll audit triggers" that allow them to rescind coverage if a post-loss audit reveals misclassification. This has led to a hardening of the excess liability market, with rates increasing by 15–25% for construction risks.

The data also shows that GCs with multiple subcontractors are more likely to face disputes. Firms with more than 10 subcontractors on a single project have a dispute rate of 18%, compared to 6% for those with fewer than 5. The complexity of tracking payroll across multiple entities is a key driver.

Another data point: a 2023 analysis by a major broker found that among disputed layers, the average premium adjustment (retroactive) was roughly $45,000, while the average legal cost was $180,000—four times the premium adjustment. This asymmetry suggests that even small misclassifications can trigger disproportionate costs, making prevention critical.

What underwriters can do to prevent payroll log fights

Underwriters can take several steps to reduce the risk of payroll log disputes. First, require quarterly payroll certifications from the insured, not just annual audits. This allows for early detection of misclassification. Second, use third-party audit firms pre-binding to verify payroll classifications. Some carriers now mandate an independent audit before binding any excess layer above $20 million.

Third, write an exclusion for subcontractor payroll entirely. This forces the GC to rely on the subcontractor's own coverage and eliminates the classification issue. However, this may leave gaps if the subcontractor's coverage is insufficient. Fourth, set attachment points based on audited payroll rather than estimated payroll. This reduces the risk of post-loss adjustments.

Fifth, include an arbitration clause specifically for audit disputes. This can speed resolution and reduce legal costs. Some policies now specify that arbitration must occur within 90 days of the dispute arising. Sixth, consider using a parametric trigger based on payroll thresholds. For example, if the audited payroll exceeds the reported payroll by more than 10%, the attachment point adjusts automatically.

Finally, underwriters should educate insureds on the importance of accurate payroll classification. Many GCs are unaware of the risks of misclassification. A simple checklist at binding can help. The market is moving toward greater transparency, with similar audit-driven pricing shifts being seen in other lines.

Underwriters should also weigh the trade-offs of different approaches. For example, requiring pre-binding audits may increase upfront costs and delay binding, but it can reduce the probability of a dispute by an estimated 40–60%, according to a 2025 carrier survey. Conversely, relying solely on annual audits may save time but expose the carrier to post-loss adjustments that are more costly to resolve.

The market move: carriers tightening payroll definitions

The dispute has accelerated a broader market trend: carriers are tightening payroll definitions and requiring more granular data. ISO has proposed new classification codes specifically for subcontractor payroll, separating it from employee payroll. Lloyd's syndicates now require a breakdown of payroll by class code at binding, and some have introduced minimum premium adjustments for misclassification.

Insurtech solutions are emerging to address the problem. Some startups offer wage data APIs that automatically classify payroll based on job titles and industry codes. These tools can reduce misclassification rates by up to 30%, according to vendor claims. However, adoption is slow due to cost and integration challenges.

Self-insured retention floors are also being adjusted. Some carriers now require a minimum SIR of $500,000 for construction risks with subcontractor payroll, up from $250,000. Brokers advise clients to purchase separate sub-limits for subcontractor liability, rather than relying on the GC's umbrella.

The market is not uniform. Some carriers are still willing to accept subcontractor payroll at face value, especially for small contractors. But the trend is clear: the days of loose payroll classification are ending. The Texas case is a warning that a single payroll log entry can unravel a $25 million layer. For underwriters, the lesson is to verify, verify, verify. For insureds, the lesson is to classify accurately—or face a gap.

Looking ahead, we may see the emergence of standardised payroll audit protocols, similar to those in workers' compensation. Some industry groups are advocating for a universal classification system that ties payroll codes to specific job tasks, reducing ambiguity. If adopted, such a system could lower dispute rates and stabilise excess liability pricing for construction risks.

This article is for informational purposes only and does not constitute professional insurance or legal advice. Readers should consult qualified professionals for guidance specific to their circumstances.