D&O Premium Flow Splits Between London Excess Layer and US Primary Market

For years, the directors and officers (D&O) liability insurance market followed a familiar pattern: US carriers wrote the primary layer, and London excess markets filled in above a certain attachment point. But that pattern is shifting. In the 2025–2026 renewal cycle, a growing share of total D&O premium is flowing to London excess layers, driven by rate divergence, regulatory friction, and the rising frequency of large securities class actions. The result is a market structure where buyers pay more for the top-end protection, while primary rates soften. This article traces the premium flow, the forces behind it, and what buyers should watch in the coming renewals.

Why London Excess Layers Are Taking a Bigger Slice of D&O Premium

The US primary D&O market has been in a corrective phase since the sharp hardening of 2020–2022. By late 2024, primary rates had begun to soften, with some estimates showing declines of 5–10% through 2025 and into 2026. Carriers that had aggressively raised rates during the pandemic era are now competing for market share, especially on low-attachment layers that cover smaller, less volatile risks. This softening has squeezed primary carriers' margins, prompting them to cede more risk to reinsurers and excess markets.

Meanwhile, London excess carriers—particularly Lloyd's syndicates and London company market players—have taken a different stance. Facing a string of large D&O claims, including securities class actions with settlements exceeding $100 million, London underwriters have firmed rates on excess layers by 10–15% in the same period. They argue that the frequency of nuclear verdicts in US courts, combined with expanded liability theories under SEC cybersecurity rules and ESG-related exposures, justifies higher pricing for the top-end coverage that attaches above $25 million or $50 million.

Brokers report that London excess markets are more willing than US carriers to write tail coverage—the extended reporting period that protects directors after a policy is cancelled or non-renewed. This flexibility has become a key selling point, especially for firms facing long-tail securities claims that can take years to surface. The appointment of Carpenter's Summers as CEO of Global Specialties at Willis Re in mid-2026 signaled a strategic shift toward specialty excess lines, reinforcing the market's focus on this segment.

Regulatory divergence further amplifies the demand for London excess layers. The US Securities and Exchange Commission's cybersecurity disclosure rules, effective from 2024, require rapid reporting of material incidents, increasing the risk of shareholder lawsuits. In contrast, the UK Financial Conduct Authority's Consumer Duty, while focused on retail outcomes, creates separate disclosure obligations for UK-listed firms. For global companies, the interplay of these regimes means that a single event can trigger claims in multiple jurisdictions, making worldwide coverage—a standard feature of London excess policies—more valuable.

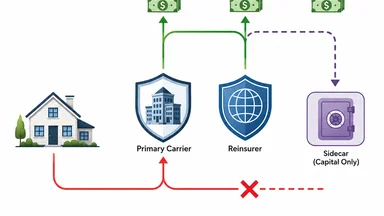

The Premium Flow Mechanics: How Ceded Business Shapes the Split

To understand the premium split, it helps to follow the money. A typical D&O program for a mid-cap US-listed company might have a $50 million total limit. The primary layer, often $10 million, is placed with a US carrier. Above that, the $40 million excess layer is split among several carriers, with a significant portion placed in London. According to a 2025 survey by the Council of Insurance Agents & Brokers, primary carriers cede roughly 30–40% of their D&O risk to reinsurers, much of which ends up in London through Lloyd's syndicates or London-based reinsurers.

Reinsurance recoveries from Lloyd's syndicates have historically been a reliable source of capacity for US primary carriers, but the terms have tightened. Gallagher Re's recent study on restricted AI models and opaque benchmarks notes that underwriters are struggling to price complex risks accurately, leading to more conservative attachment points. In D&O, this means that London excess layers command 20–30% of the total premium pool, even though they cover only the top half of the limit structure. The exact share varies by risk, but the trend is upward: in 2024, London's share of US-originated D&O premium was estimated at around 25%, up from roughly 20% three years earlier.

Attachment points on London excess layers typically range from $25 million to $50 million for mid-cap risks, though they can be as low as $10 million for smaller firms or as high as $100 million for large caps. The premium for these layers is priced as a rate-on-line—the premium as a percentage of the limit—which has been rising. Brokers report that London syndicates are quoting rate-on-line figures 20–25% lower than US excess markets for the same attachment point, partly because London carriers have more diversified portfolios and partly because they are willing to take on more tail risk. This pricing advantage, however, comes with stricter terms, including narrower definitions of "claim" and more robust fraud exclusions.

The opacity of pricing models in the D&O market adds to the challenge. Gallagher Re's report highlights that restricted AI models and unreliable benchmarks are undermining insurers' ability to price AI-related risks, but the same could be said for D&O exposures tied to cybersecurity and ESG. Without transparent data on claims frequency and severity at different attachment points, buyers must rely on broker expertise and market intelligence to gauge whether London excess pricing is fair.

Rate Divergence: US Primary Softening vs London Firming

The most visible driver of the premium split is the rate divergence between the two markets. US primary D&O rates have been softening since mid-2023, with some observers reporting declines of 5–10% year-over-year through the first half of 2026. This softening reflects increased competition among US carriers—AIG, Chubb, and others have been vying for market share on primary layers, particularly for accounts with clean loss histories. The entry of new capacity from alternative capital providers and insurtechs has also put downward pressure on rates.

In contrast, London excess rates have been firming, with increases of 10–15% over the same period. The frequency of large claims—those exceeding $25 million—has been a key factor. Securities class actions, in particular, have become more common and more expensive. The average settlement in 2025 was roughly $35 million, up from around $25 million five years earlier, according to data from Cornerstone Research. Nuclear verdicts in US courts, where juries award damages in the hundreds of millions, have also driven demand for higher attachment points, as primary layers alone cannot cover such exposures.

The FBI's alert on rising cargo theft, while not directly a D&O issue, illustrates the broader liability cost pressure that affects excess layers. As supply chain risks multiply, directors and officers face increased scrutiny for oversight failures. A product recall like Stellantis's 2026 recall of 1.3 million Jeep SUVs due to fire concerns—urging owners to park outside—can trigger D&O claims if shareholders allege that management failed to address safety issues in a timely manner. These spillover effects from product liability into D&O are pushing excess carriers to raise rates.

Some US carriers, notably AIG and Chubb, have pulled back on writing low-attachment excess layers in London, preferring to focus on primary and first-excess positions in their home market. This has created a vacuum that London specialists are filling, but at higher prices. The result is a bifurcated market: buyers can get cheaper primary coverage, but they must pay more for the peace of mind that comes with high-limit excess protection.

The Regulatory Friction That Redistributes Premium

Regulatory divergence across jurisdictions is a powerful force reshaping D&O premium flows. The SEC's cybersecurity rules, which took effect in 2024, require US-listed companies to disclose material cybersecurity incidents within four business days. This tight timeline increases the risk of premature or inaccurate disclosures, which can lead to shareholder lawsuits. As a result, US firms are buying higher D&O limits—often $50 million or more—to cover potential securities claims arising from cyber events. The primary layer may cover the first $10 million, but the excess layers, often placed in London, absorb the rest.

Across the Atlantic, the UK FCA's Consumer Duty, implemented in 2023, imposes a new standard of care on firms that sell financial products. While not directly targeting D&O, it creates separate disclosure risks for UK-listed firms, particularly those with retail customer bases. A failure to ensure fair value could lead to regulatory fines and shareholder actions. London excess policies typically include worldwide coverage, making them a natural fit for global firms that need protection across multiple regulatory regimes.

The EU's Corporate Sustainability Reporting Directive (CSRD), phased in from 2024, adds another layer of complexity. It requires companies to report on ESG risks, including environmental and social impacts, with third-party assurance. Directors who sign off on inaccurate or misleading ESG disclosures could face liability under both securities laws and broader corporate governance standards. US primary policies often exclude ESG-related claims or offer limited coverage, while London excess policies have begun to include specific ESG endorsements—at an additional premium.

This regulatory arbitrage keeps premium flowing across the Atlantic. A US company with European subsidiaries may find that its US primary policy does not cover exposures under the CSRD or FCA rules, forcing it to buy a London excess policy that fills the gap. Conversely, a UK company with US listings may need the higher limits and broader coverage that London markets offer for US securities class actions. The net effect is a transatlantic premium flow that tilts toward London for excess layers, as buyers seek to harmonize their coverage with the most onerous regulatory requirements.

Case Study: How a Mid-Cap Tech Firm's D&O Program Splits

To illustrate the mechanics, consider a hypothetical mid-cap technology firm based in the US, with annual revenues of roughly $2 billion and a market capitalization of $5 billion. The firm faces typical D&O exposures: shareholder lawsuits over earnings guidance, cybersecurity incidents, and potential IP litigation. Its risk manager, working with a broker, designs a $50 million D&O program.

The primary layer of $10 million is placed with a US carrier, such as Chubb or AIG, at a rate of roughly 5–7% of limit, translating to a premium of around $500,000 to $700,000. The broker then shops the remaining $40 million excess layer. A US excess carrier quotes $30 million at $25 million attachment for a rate-on-line of 4%, or $1.2 million. But a London syndicate offers the same $30 million layer at a rate-on-line of 3.2%, or $960,000, with the added benefit of tail coverage and worldwide wording. The broker recommends the London placement, and the firm saves roughly $240,000 while gaining broader coverage.

The premium split in this example is roughly 40% primary ($600,000) and 60% excess layers ($1.6 million), with the London share representing about 37% of the total premium. The broker's commission structure may favor the excess placement, as commissions on London excess layers can be higher—sometimes 10–15% of premium, compared to 7–10% on primary. This creates an incentive for brokers to steer business toward London excess markets, though buyers should verify that the coverage terms justify the shift.

The case study also highlights the importance of attachment points. If the firm had a clean loss history, it might negotiate a lower attachment point—say $20 million—which would make the excess layer cheaper. But with the market firming, London syndicates are less willing to drop attachment points, especially for tech firms with elevated cyber risk. The buyer must weigh the cost savings against the risk of exhausting the primary layer and self-insuring the gap.

Data from a 2025 report by Advisen suggests that mid-cap tech firms are increasingly opting for London excess layers, with the share of total premium allocated to London rising from 22% in 2022 to 28% in 2025. This trend is most pronounced for firms with revenues above $1 billion, where the complexity of exposures and the need for tail coverage make London markets more attractive. For smaller firms, the cost savings may not outweigh the additional negotiation effort, but the overall direction is clear.

What Buyers Should Watch in the Next Renewal Cycle

As the 2026–2027 renewal season approaches, buyers should monitor several trends in the London excess market. First, attachment points are likely to continue rising, particularly for firms in sectors with high litigation risk, such as technology, healthcare, and financial services. London syndicates are signaling that they will not write excess layers below $30 million for mid-cap risks, and some are targeting $50 million as the new floor. Buyers should negotiate early and consider multi-year deals to lock in current attachment levels.

Second, tail coverage is becoming a critical differentiator. Securities class actions can take years to resolve, and a policy that does not include adequate tail coverage may leave directors exposed after a merger, acquisition, or change in carrier. London markets are more willing to offer multi-year tail options, often at a premium of 50–75% of the annual rate. Buyers should compare tail provisions across markets and factor them into the total cost of the program.

Third, the spillover from product liability into D&O is a growing concern. A product defect can trigger shareholder lawsuits alleging that directors failed to oversee safety protocols. Buyers should ensure that their D&O policies do not exclude claims arising from product liability, or if they do, that they have separate product liability coverage that fills the gap. The Stellantis recall, which affected over 1.3 million vehicles, serves as a reminder that even well-managed companies can face D&O exposure from product safety issues.

Fourth, the rise of AI model risk assessments may reshape underwriting by 2027. Gallagher Re's report warns that restricted AI models and opaque benchmarks are undermining insurers' ability to price risk accurately. For D&O, this could mean that carriers rely more on qualitative assessments and less on data-driven models, leading to wider rate variability. Buyers should work with brokers to present a clear risk narrative, including cybersecurity controls, ESG disclosures, and governance practices, to secure the best terms.

Finally, buyers should consider the potential for a market correction. If large claims frequency stabilizes or if new capacity enters the London excess market, rates could soften. However, given the structural drivers—regulatory divergence, nuclear verdicts, and the demand for tail coverage—a significant reversal seems unlikely in the near term. Buyers who lock in multi-year deals now may benefit from current pricing, while those who wait could face higher costs.

Will the London excess market continue to capture a growing share of D&O premium, or will US carriers adapt by offering more competitive excess terms? The answer depends on how quickly US carriers can match the flexibility and coverage breadth of London markets. For now, the trend favors London, but buyers should stay alert to shifts in capacity and pricing that could alter the balance.

Disclaimer: This article is for informational purposes only and does not constitute professional advice. Readers should consult qualified insurance brokers and legal advisors for guidance tailored to their specific circumstances.