Auto Telematics Claim Denied Over GPS Timestamp Log Discrepancy

A policyholder filed a claim after a rear-end collision at a signaled intersection. The telematics device installed under the insurer's usage-based program recorded the vehicle's speed, location, and time. The insurer's claims system flagged a 47-second gap between the impact timestamp and the GPS log entry. The denial letter cited a timestamp mismatch as grounds to reject coverage, arguing the data did not corroborate the accident as reported. The policyholder insists the device calibration was off. The internal adjuster review is now under way.

Telematics Claim Denial: A Disputed GPS Timestamp

The policyholder submitted a first notice of loss within 24 hours of the accident, as required by the telematics policy terms. The insurer's automated system pulled the GPS log and compared it against the police report and the device's accelerometer data. The discrepancy amounted to roughly 47 seconds—the GPS timestamp lagged behind the collision event recorded by the accelerometer. The adjuster handling the case noted that the policy's fine print requires timestamp alignment within a small tolerance for coverage to apply.

The denial letter, issued 30 days after the claim was filed, stated that the timestamp mismatch violated the telematics data integrity clause. The policyholder countered that the device had shown intermittent calibration errors in the months prior, though no formal complaint was filed. The adjuster reviewed the device's maintenance log and found no recorded calibration alerts. The case now hinges on whether the device error is plausible or the data is accurate.

Internal adjuster review involves re-examining the raw data logs and consulting with the telematics vendor. The adjuster must decide whether to uphold the denial or recommend an exception. In practice, such disputes are rare but growing as telematics adoption increases. Some carriers have begun including arbitration clauses for data disputes, but this policy did not. The outcome will set a precedent for how the insurer handles similar claims going forward.

To understand how typical such a gap is, consider that telematics devices from different manufacturers have varying GPS sampling rates. Some units log position every second, while others sample at intervals of up to 15 seconds. A 47-second gap might be abnormal for a high-frequency device but could be within normal operation for a low-cost unit. The policy in question did not specify the device's sampling rate, leaving room for interpretation. A similar dispute in a neighboring state was resolved in favor of the policyholder after an independent audit revealed that the device's GPS module had a known firmware bug causing intermittent dropouts. That case settled for the full claim amount plus legal costs. The current carrier is aware of that precedent and may factor it into the review.

How Telematics Data Flows Into Claims Decisions

The telematics device in this case is a plug-in unit that records speed, location, and time at intervals of roughly one second. Data is uploaded to the insurer's cloud platform each time the vehicle is turned off. The claims system automatically cross-references the logs against the reported accident time and location. A rule engine flags any outlier—such as a timestamp gap exceeding a set threshold—for human review.

The human adjuster then validates or overrides the flag. In this instance, the adjuster saw the 47-second gap and requested the full data log from the vendor. The log showed that the device had not recorded any GPS coordinates for the 47-second window, but the accelerometer data indicated a sudden deceleration consistent with a collision. The adjuster weighed the reliability of each data stream.

Telematics vendors typically provide a data accuracy guarantee, but the policy's terms give the insurer discretion to interpret data gaps. The adjuster noted that the device had a firmware update three weeks before the accident, which could have caused a temporary glitch. However, the vendor's logs showed no error codes. The case illustrates the tension between automated flagging and human judgment.

Some industry observers argue that telematics data should be treated as presumptive evidence, while consumer advocates insist on independent verification. The NAIC has issued guidance urging insurers to disclose data collection practices and provide policyholders access to their own logs. In this case, the policyholder only received a summary report, not the raw data.

The data flow architecture itself introduces latency. The device stores data locally and transmits it in batches when the ignition is off. If the accident occurred mid-trip, the GPS log for the collision moment might not have been uploaded until hours later, but the timestamp is recorded at the device level. The 47-second gap could be due to a buffer overflow or a temporary loss of satellite signal, especially if the vehicle was in a parking garage or under a bridge. The adjuster's report did not mention whether the location was an urban area with tall buildings, which can cause GPS multipath errors. This omission may be relevant to the appeal.

The Business of Telematics: Premium Flow and Risk Selection

Usage-based insurance policies typically offer premium discounts of 10 to 30 percent for safe driving behavior. The insurer collects granular data on mileage, speed, braking, and time of day. This reduces adverse selection by attracting lower-risk drivers who are willing to share data. The premium flow for telematics books is more predictable because risk is assessed in near-real time.

For the carrier, telematics improves loss ratios by rewarding safe drivers and identifying high-risk behavior early. Some estimates place the loss ratio improvement for telematics portfolios at roughly 5 to 10 points compared to traditional books. The savings are shared with policyholders through lower premiums, but the trade-off is data transparency and the risk of claim disputes like this one.

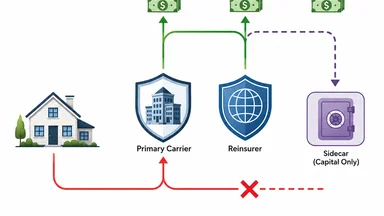

The premium collected from telematics policies is often ceded to reinsurers under quota-share treaties. Reinsurers require detailed loss data to price the risk. A timestamp discrepancy can complicate the cession process because the reinsurer may question the validity of the claim. If the claim is denied, the primary insurer retains the premium but faces potential bad-faith litigation.

Brokers play a key role in advising clients on telematics policies. They should verify the coverage triggers and data accuracy guarantees. Some brokers recommend independent data audits for high-value claims. The growing telematics market—expanding at roughly 15 percent annually—means more policyholders will encounter these issues.

The economics of telematics also involve customer acquisition costs. Insurers often subsidize the device hardware and installation, expecting to recoup the expense through reduced claims over the policy lifetime. A single disputed claim can erode that margin. For a policy with an annual premium of around US$800, the device cost might be US$50–100. If the claim is for US$5,000 and the denial is overturned, the insurer not only pays the claim but also incurs legal fees and potential regulatory fines. Some carriers have begun setting aside reserves specifically for telematics-related disputes, a practice that is still uncommon in traditional auto lines.

Reinsurance Recoveries and the Timestamp Gap

When a telematics claim is ceded to a reinsurer, the ceding insurer must provide precise loss details, including the timestamp of the accident. The reinsurer's underwriting guidelines often require GPS log confirmation within a certain tolerance. A 47-second gap may be enough to trigger a coverage dispute between the primary insurer and its reinsurer.

In this case, the primary insurer's quota-share treaty with a major reinsurer includes a clause that allows the reinsurer to deny recovery if the claim data is inconsistent. The reinsurer has requested the full data log and may conduct its own audit. If the reinsurer refuses to indemnify, the primary insurer bears the full loss amount, which could be substantial.

The financial impact extends beyond the single claim. If the reinsurer flags a pattern of data issues, it may demand higher ceding commissions or tighter data standards. Some carriers have responded by investing in data validation tools that cross-check telematics logs against third-party sources like traffic cameras or police reports.

Industry practice is evolving. A recent report by a consulting firm noted that reinsurers are increasingly hiring data auditors to review telematics claims. The cost of such audits is typically passed back to the primary insurer. For smaller carriers, the expense may outweigh the benefit of telematics programs. The trend mirrors broader scrutiny of data-driven underwriting.

Consider a hypothetical scenario: A reinsurer audits a block of telematics claims and finds that 3 percent have timestamp gaps of 30 seconds or more. The reinsurer might impose a penalty of 10 percent on the ceding commission for that block. For a US$10 million premium book, that penalty amounts to US$1 million—a significant hit to the primary insurer's profitability. To avoid such outcomes, some carriers have set internal thresholds: if a claim's timestamp gap exceeds 60 seconds, the claim is automatically escalated to a senior adjuster before any denial is issued. This case's 47-second gap falls just below that threshold, which may be why it was handled by a standard adjuster.

Claims Handling Timeline: From First Notice to Final Decision

The timeline for this claim began with the first notice of loss within 24 hours. The insurer's system automatically flagged the timestamp discrepancy on day two. The adjuster requested the full data log on day three, but the vendor took two business days to deliver it. By day seven, the adjuster had reviewed the log and consulted with the telematics vendor's support team.

State regulations require insurers to issue a coverage decision within 30 days of the claim filing. The denial was sent on day 28. The policyholder has 45 days to appeal under the policy terms. The appeal process involves a second adjuster review and potentially an independent data expert. The timeline for a final decision could extend to 90 days.

During the appeal, the policyholder's attorney may request the raw data logs and the device's calibration history. The insurer must produce these documents under state discovery rules. The cost of litigation can quickly exceed the claim amount, especially for a mid-sized loss. Some carriers opt to settle borderline cases to avoid legal expenses, but this carrier has a reputation for strict enforcement.

The timeline highlights the tension between efficiency and fairness. Automated systems speed up initial triage but can create rigid outcomes. Human adjusters have discretion but may be influenced by carrier culture. The industry is debating whether to mandate a cooling-off period for telematics-based denials or require a second review before issuance.

Comparative data from a recent industry survey shows that the average time to resolve a telematics dispute is 72 days, compared to 45 days for traditional claims. The extra time is often due to data retrieval and expert review. For the policyholder, this delay can mean weeks without a rental car or repair funds. Some states, like California, have proposed regulations that would require insurers to advance partial payments for proven losses while the dispute is pending. If adopted, such rules could shift the balance of power in data disputes.

Industry Context: Telematics Adoption and Regulatory Pushback

Telematics policies now account for roughly 15 percent of the U.S. auto insurance market, up from about 5 percent a decade ago. Adoption is driven by consumer demand for lower premiums and insurer appetite for better risk data. However, regulatory scrutiny is increasing. Several states have introduced bills requiring insurers to disclose how telematics data is used and to allow policyholders to correct errors.

The NAIC adopted a model act on telematics fairness in 2025, which recommends that insurers provide policyholders with access to their raw data and a process to dispute inaccuracies. The model act also suggests that insurers cannot deny a claim solely on telematics data without corroborating evidence. This case tests that principle.

Consumer advocates argue that telematics devices can have calibration errors, especially after firmware updates. They point to studies showing that GPS accuracy can degrade in urban canyons or tunnels. Insurers counter that telematics data is more objective than human testimony and reduces fraud. The debate mirrors earlier disputes over credit-based insurance scores.

The outcome of this claim could influence regulatory developments. If the denial is upheld, consumer groups may push for stricter rules. If overturned, insurers may tighten data validation protocols. The industry is watching closely.

Looking at international parallels, the European Union's General Data Protection Regulation (GDPR) has already forced some telematics providers to give policyholders full access to their data. In the UK, the Financial Ombudsman Service has handled several cases where timestamp gaps were deemed insufficient to deny coverage. In one 2023 case, the ombudsman ruled that a 90-second gap did not invalidate the claim because the accelerometer data corroborated the collision. That ruling is often cited by policyholder attorneys in the U.S. as persuasive authority, even though it is not binding. The current carrier's legal team is likely aware of this precedent.

Practical Takeaways for Policyholders and Brokers

Policyholders with telematics devices should review the device installation and ensure it is functioning properly. Any calibration issues should be documented and reported to the insurer immediately. Keeping a log of device behavior can support a future dispute. The policyholder in this case had no written record of prior glitches.

Brokers advising clients on telematics policies should verify the coverage triggers and data accuracy guarantees in the policy language. They should also discuss the possibility of data disputes and recommend that clients request full data logs after any accident. Some brokers now include an independent data audit clause in their service agreements.

If a claim is denied based on telematics data, policyholders should request the raw data logs and the device's calibration history. An independent expert can review the logs for errors. The cost of an audit may be recoverable if the denial is overturned. Legal counsel experienced in telematics disputes can help navigate the appeals process.

The broader lesson is that telematics insurance offers benefits but also introduces new risks. The data that lowers premiums can also be used to deny coverage. Policyholders and brokers must stay informed about how data is collected, stored, and interpreted. As the market grows, so will the number of disputes like this one.

For brokers, a practical step is to maintain a list of approved independent data auditors who specialize in telematics. The fee for a basic audit is typically in the range of US$500–1,500, which is often recoverable if the claim is paid. Some broker networks have negotiated preferred rates with audit firms. Including a clause in the broker agreement that requires the insurer to reimburse audit costs if the denial is overturned can protect clients and reduce friction.

Policyholders should also be aware that telematics data can be used against them in subrogation. If the data shows the policyholder was at fault, the insurer may pursue recovery from a third party. Conversely, if the data is ambiguous, it could weaken the subrogation case. In this instance, the timestamp gap might affect the ability to recover from the other driver's insurer. The policyholder's attorney should consider this angle.

This article is for informational purposes only and does not constitute legal or professional advice. Policyholders and brokers should consult with qualified professionals regarding specific claims or coverage questions.