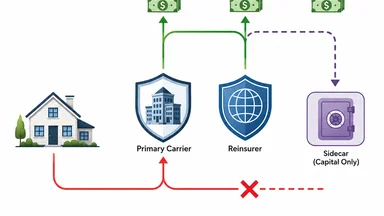

Claim Payment Stops at Reinsurance Sidecar While Primary Carrier Nets Premium

When a homeowner buys a property insurance policy, the premium they pay is just the start of a long financial journey. That money moves upstream through a chain of intermediaries—primary carriers, reinsurers, and finally into vehicles called sidecars, which are special-purpose entities that hold capital but have no obligation to pay claims directly. The result is a structural mismatch: premiums flow quickly to investors, but claim payments can stall for months or years while each layer of the chain verifies, audits, and disputes. This article traces that money trail, using recent events to show how the design of reinsurance sidecars can leave policyholders waiting while carriers and investors earn returns.

Premium Flows Upstream, Claims Stop at the Sidecar

The basic economics of property insurance are straightforward on the surface. A policyholder pays a premium to a primary carrier, which retains a portion of the risk and cedes the rest to a reinsurer under a quota-share treaty. The reinsurer, in turn, may retrocede part of that risk to a sidecar—a special-purpose vehicle funded by institutional investors seeking uncorrelated returns. The sidecar earns a share of the premium for assuming the risk, but it has no claims department, no adjusters, and no direct obligation to pay policyholders.

When a loss occurs, the primary carrier must pay the claim from its own surplus first, then seek reimbursement from the reinsurer. That recovery can take months, as the reinsurer reviews the claim for compliance with the treaty. The sidecar, sitting at the top of the chain, is even further removed: its only job is to hold collateral and release it per the contract, but that release depends on the reinsurer confirming the loss. Policyholders, meanwhile, are left waiting for a payment that has to travel back down the chain.

The timeline is rarely transparent to the insured. According to a 2023 study by the Insurance Information Institute, the average time to settle a non-catastrophe homeowners claim is approximately 45 days for carriers with strong financial ratings, but claims involving reinsurance layers can extend to 90-120 days. For catastrophe claims, the timeline can stretch to six months or more, especially when sidecars are involved. The primary carrier has little incentive to expedite the recovery, since it has already collected the premium and may be earning investment income on the float.

Sidecar investors, by contrast, are indifferent to claim speed. Their return is based on premium share minus losses, but they have no servicing obligation. This creates a fundamental asymmetry: the premium flows upstream quickly, but the claim payment must fight its way back down through a chain where no single entity is responsible for speed.

The Sidecar Mechanics: Capital Without Service

A reinsurance sidecar is not an insurer in the traditional sense. It is a special-purpose vehicle, typically structured as a collateralized reinsurer, that provides capacity for peak risks—catastrophe exposures, large property lines, or aggregate excess layers. Investors, often pension funds or hedge funds, contribute capital in exchange for a share of the premium and a defined loss exposure. The sidecar has no employees, no claims department, no adjusters, and no call center. Its only function is to hold capital and release it according to a pre-negotiated contract.

When a claim arises, the primary carrier must pay from its own surplus first. If the carrier is thinly capitalized, that payment may be delayed while it negotiates with the reinsurer. The reinsurance recoverable—the amount the primary expects to collect from the sidecar—becomes an asset on the primary's balance sheet. But that asset is only as good as the sidecar's willingness to pay, and the sidecar's obligation is triggered only after the reinsurer certifies the loss.

The sidecar's contract typically includes strict documentation requirements: proof of loss, coverage analysis, and sometimes third-party audits. These requirements are designed to protect investors, but they also create friction. The primary carrier's adjuster must satisfy not just one set of standards, but potentially two or three, depending on the number of layers. Each layer can demand additional information, and disputes over interpretation can stall payment indefinitely.

This structure is efficient for investors—they get premium income without operational overhead—but it shifts the burden of speed onto the primary carrier. If the primary carrier is well-capitalized and efficient, claims are paid quickly. If it is stretched, the policyholder bears the cost of the delay. The sidecar itself has no incentive to speed up the process, since its return is not tied to claim settlement time.

Maui Wildfire Settlement Shows the Timing Trap

The Maui wildfire of August 2023, which destroyed much of Lahaina, generated an estimated $4.03 billion in insured losses. In June 2026, Hawaiʻi Circuit Judge Peter Cahill capped legal fees for the settlement at $222 million, a fraction of the $1 billion sought by plaintiffs' attorneys. But for insurers, the timeline of payments tells a different story.

Primary carriers fronted payments to policyholders within months of the fire, drawing on their own surplus. However, reinsurance recoveries from multiple layers—including sidecar vehicles—took years to materialize. Litigation over subrogation and allocation of losses further delayed final settlements. Some carriers reported that they had not fully collected on their reinsurance recoverables as of early 2026, nearly three years after the event.

The sidecar investors in the Maui wildfire were not directly involved in the settlement negotiations. Their exposure was defined by the contract, and they had no obligation to pay policyholders directly. Instead, they waited for the primary carriers to submit claims, audit them, and release funds. During that waiting period, the sidecar capital continued to earn investment returns, while policyholders who had already been paid by their insurers faced delays in final resolution of their claims.

The Maui case is not unique. Catastrophe events often expose the gap between premium flow and claim payment. For sidecar investors, the delay is a feature, not a bug: it allows them to hold capital longer and earn more income. For policyholders, it is a hidden cost that most never see.

Parametric Triggers Offer a Faster Path, But Not for All

In June 2026, Descartes Underwriting partnered with Nextpower to launch a parametric wind insurance solution for solar power plants. The product uses site-level wind data from Nextpower meteorological stations to trigger payments automatically when straight-line wind speeds exceed a threshold, bypassing the traditional loss adjustment process. Because parametric insurance pays on an index rather than actual loss, the sidecar can release funds almost instantly—no adjuster, no audit, no delay.

Parametric insurance has been growing in popularity for specific perils, particularly in renewable energy and agriculture. For a solar plant operator, a parametric wind policy can provide liquidity within days of a storm, allowing repairs to begin immediately. The sidecar structure works well here because the trigger is objective and verifiable, reducing the need for claims investigation.

But parametric covers only named perils with clear indices. Most homeowners policies remain indemnity-based, meaning they pay based on actual loss, not a proxy. For a typical property claim—fire, theft, liability—the adjuster must inspect, document, and estimate. That process cannot be automated with a weather station. As a result, the vast majority of property insurance claims remain subject to the traditional chain of payment delays.

Indiana Farmers Insurance CEO Wes Sprinkle, in a June 2026 interview with Carrier Management, described a different path: using AI to speed claims processing without changing the underlying insurance structure. AI can accelerate documentation review and fraud detection, but it does not alter the fundamental flow of money through reinsurance layers. Parametric solutions offer a structural fix, but only for a narrow slice of risks.

China Evergrande's Fall Exposes Reinsurance Counterparty Risk

The liquidation of China Evergrande Group, the collapsed property developer, sent shockwaves through global reinsurance markets. As reported by Insurance Journal in June 2026, some partners at PwC's Hong Kong and mainland China affiliates began weighing asset shielding amid concerns about liability. For insurers with exposure to Evergrande, the default raised a different question: what happens when a primary carrier cannot collect from its reinsurer?

Evergrande's collapse cascaded to insurers that had written property coverage on its developments. Some of those insurers had ceded risk to Chinese sidecar vehicles, which were themselves exposed to the developer's insolvency. When the primary carriers attempted to recover from the sidecars, they faced collectability doubts: the sidecar's collateral was tied up in litigation, and the sidecar's investors were reluctant to release funds without certainty.

The result was that primary carriers in Hong Kong had to pay claims from their own surplus, with no guarantee of full recovery. Policyholders who had bought insurance on Evergrande properties found themselves waiting for payments while the carriers fought to salvage their reinsurance recoverables. The sidecar structure, designed to insulate investors from operational risk, offered no protection against the cedent's insolvency.

This case illustrates a broader lesson: sidecar capital is only as good as the primary carrier's survival. If the primary carrier becomes insolvent or faces liquidity pressure, the sidecar's obligation to pay becomes moot. Policyholders are left with a claim against a carrier that may not have the funds to pay, while the sidecar investors walk away with their capital intact.

How Adjusters Navigate the Payment Chain

For the adjuster in the field, the reinsurance sidecar is an invisible constraint. The adjuster's job is to document the loss thoroughly enough to satisfy not just the primary carrier, but also the reinsurer and, indirectly, the sidecar's auditors. Each layer may have its own requirements: proof of loss forms, coverage analysis, photographs, estimates, and sometimes third-party engineering reports.

Experienced adjusters know that the documentation must be airtight to avoid delays in the recovery chain. A missing signature or an ambiguous estimate can trigger a request for additional information, which can add weeks to the process. The adjuster works under time pressure from the policyholder, who wants payment quickly, but also must meet the standards of distant investors who have never seen the property.

Sidecar investors rarely see individual claims; they rely on aggregate reports from the reinsurer. But if a particular claim is large enough to trigger the sidecar's attachment point, it may be subject to special scrutiny. The adjuster may be asked to provide a detailed narrative of the loss, including the cause, the extent of damage, and the basis for the estimate. Any ambiguity can be exploited to delay payment.

Best practice for adjusters is to communicate early and often with the policyholder about the expected timeline. If the claim involves a large loss that will go to reinsurance, the adjuster should explain that the payment may take longer than a standard claim. Transparency can reduce frustration, but it cannot eliminate the structural delay built into the system.

Trade-Offs in the System: Speed vs. Capital Efficiency

The sidecar structure is not inherently flawed; it serves a purpose in the insurance ecosystem. By bringing institutional capital into the reinsurance market, sidecars increase capacity for peak risks, which can lower premiums for policyholders in catastrophe-prone areas. Without sidecars, insurers would have to retain more risk or charge higher rates to cover their exposure. The trade-off is that this capital is managed at arm's length, with no direct claims-paying obligation, which can slow payment when losses occur.

Proponents of sidecars argue that the delays are a necessary cost of accessing cheap capital. Investors demand strict documentation and audit rights to protect their funds, and that scrutiny can improve loss adjustment accuracy. In theory, fewer fraudulent or inflated claims get paid, which benefits all policyholders through lower overall loss costs. However, the burden of this scrutiny falls disproportionately on legitimate claimants who must wait longer for their payments.

Regulators have taken notice. Some state insurance departments have begun requiring carriers to disclose their reinsurance structures and expected recovery timelines in policy documents. In 2025, the National Association of Insurance Commissioners (NAIC) issued a white paper on sidecar transparency, recommending that carriers provide policyholders with a clear explanation of how reinsurance arrangements may affect claim settlement times. These measures are voluntary for now, but they signal a growing awareness of the issue.

Another trade-off involves the cost of speed. Parametric insurance, which bypasses the sidecar delay, often comes with a higher premium because the trigger is less precise and the insurer bears basis risk. For a homeowner, a parametric wind policy might cost 20-30% more than a traditional indemnity policy for the same peril. The faster payment is a benefit, but it is priced into the product. Similarly, captive arrangements require the policyholder to retain more risk and commit capital upfront, which is feasible only for large commercial entities.

The system, in other words, reflects a series of compromises between cost, speed, and capital efficiency. Policyholders who want faster claims may need to pay more or accept narrower coverage. Those who prioritize low premiums may have to tolerate longer wait times. The sidecar is one mechanism in that balancing act, and its impact on claim timing is a direct consequence of its design.

What the Policyholder Can Do When Payment Stops

When a claim payment is delayed, the policyholder's first step should be to ask the insurer directly about the reinsurance structure and the expected recovery timeline. Many carriers are willing to explain that the claim has been submitted to the reinsurer and that payment is pending. If the delay is unreasonable—beyond 60 days for a straightforward claim—the policyholder can file a complaint with the state insurance department.

In general, sidecar capital is not a claims-paying resource for policyholders. The sidecar's obligation runs to the reinsurer, which in turn owes the primary carrier. The policyholder's only contractual relationship is with the primary carrier. If the primary carrier is slow to pay, the policyholder must pursue the carrier, not the sidecar.

For businesses with large property exposures, parametric insurance or captive arrangements can offer faster claims settlement. Parametric policies pay on index triggers, bypassing the traditional adjustment chain. Captives allow the policyholder to retain more risk and reduce reliance on the reinsurance market. However, these options are not available to most homeowners, who remain dependent on the standard indemnity-based system.

Monitoring the carrier's financial ratings and reinsurance panel strength can also help. A carrier with a strong surplus and a diversified reinsurance panel is more likely to pay claims quickly, even if a sidecar is involved. In protracted disputes, the state insurance department can intervene on timeliness, but that process can itself take months.

The structure of reinsurance sidecars creates a natural tension between the interests of investors and policyholders. Premiums flow quickly to capital providers, but claims must travel back through a chain where no single entity is responsible for speed. Understanding this dynamic can help policyholders set realistic expectations and take proactive steps to protect their interests.

Disclaimer: This article is for informational purposes only and does not constitute professional insurance or legal advice. Policyholders should consult with a qualified advisor regarding their specific situation.